Illicit Financial Flows (IFFs) have gained considerable traction in the advocacy and policy sphere, with most attention directed to their damaging impact on resource-rich developing countries that rely heavily on natural resource revenues. However, significant challenges remain in the conceptual framework and appropriate measurement techniques that aim to trace, curb, and redirect public revenue lost via IFFs to overall welfare-enhancing purposes. In this article, PhD candidate Siddhant Marur discusses the current state of the literature with regards to their measurement and provide recommendations on how to improve these methods moving forward.

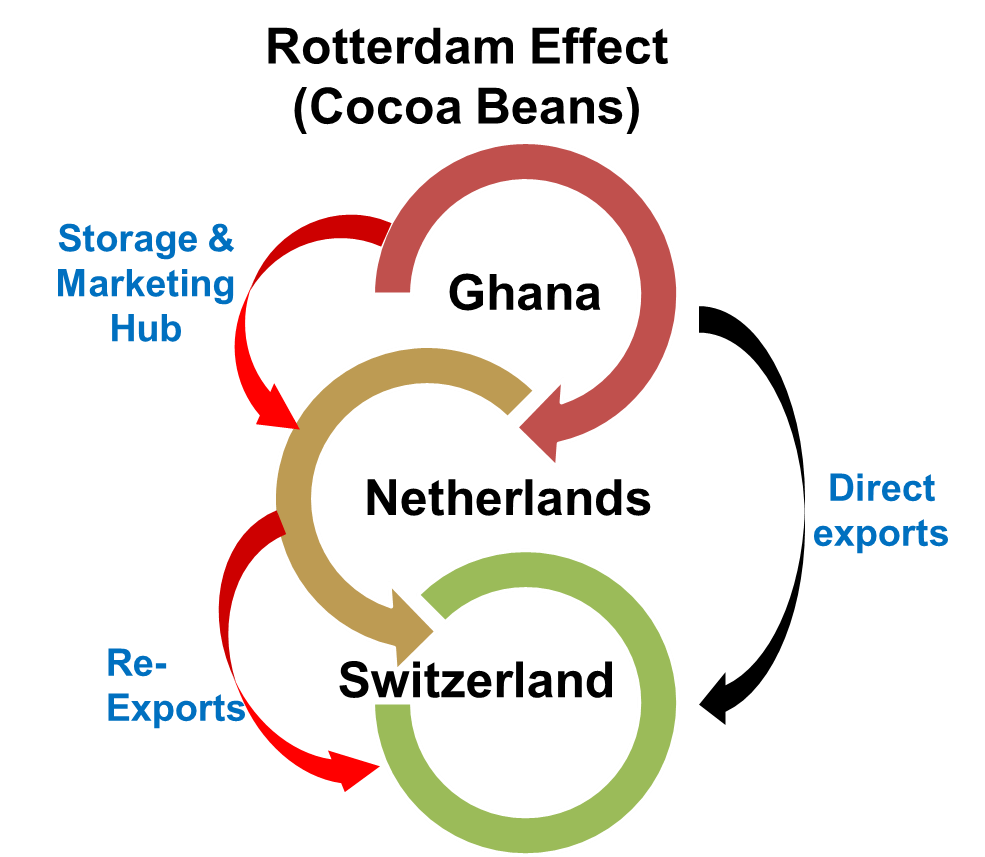

It is understandable that IFFs are inherently hard to measure due to their clandestine nature, especially those arising from illegal channels (such as smuggling, money laundering). However, IFFs arising from legal channels such as commodity trade – via trade and transfer mispricing – are usually recorded by the relevant customs authorities, providing the most useful avenue for identifying and curbing such flows. With continual improvements in the methods and data over time, multiple measurement techniques have emerged in this domain. The principal approach, commonly referred to as the Partner-Country Trade Gap (PCTG) technique, uses mirror statistics from trading partners to estimate IFFs based on asymmetries in their corresponding import-export statistics (Bhagwati, 1974). Even so, this technique’s credibility is questionable due to built-in limitations in the way customs recording practices have evolved across countries and over time. For instance, the fundamental assumption of developed countries having more reliable statistics has proven to be misguided (Hong and Pak, 2017). Coupled with incongruences arising from Entrepôt trade (such as the ‘Rotterdam effect’), which conflate trading hubs with destination countries, and country-level idiosyncrasies in commodity classification, the limitations of this technique have proven prohibitive in providing any conclusive evidence of trade mispricing (Nitsch, 2016 ; Marur 2019).

Fortunately, internationally traded commodities provide us with an important and globally verifiable benchmark- global commodity market prices. Measured against contemporaneous prices, transaction values which appear abnormally over or under priced (i.e. outside a reasonable price range) provide credible reason for investigation. This is the crux of the Price Filter Analysis method, an alternative and more recent methodology that relies on detailed country-level microdata on product-type, quantity and unit value. Relying on global transfer pricing guidelines, this methodology is motivated by the Comparable Uncontrolled Price (CUP) method for establishing the arm’s length price range for commodities using commodities exchange prices (OECD, 2017; Platform for Collaboration on Tax, 2017; United Nations, 2017). The arm’s length is defined using standardized assumptions on product heterogeneity, market conditions and transportation costs.

The limitations in this method appear to be less misleading, with issues around the generalizability of assumptions, outlier-sensitivity, and imprecise product classifications in the Harmonized Commodity Description and Coding Systems (HS) at the fore. Consequently, this technique has found increasing favor in the academic literature on estimating IFFs in commodity trade. Our empirical work applies and improves this methodology by making less arbitrary and more industry-informed assumptions on the appropriate price range around commodities including gold, coffee, and cocoa. For instance, we explicitly account for product heterogeneity in gold doré bars based on expert interviews and data which reflect the average purity of gold content arriving from different countries into Switzerland. Similarly, acknowledging that global market prices are not reflective of commodity prices for highly differentiated goods such as coffee and cocoa, we apply country-level inter-quartile range filters to arrive at the most reasonable estimates of IFFs in these commodities.

In conclusion, we find that using aggregate measurement techniques such as the PCTG with generalized assumptions can result in misleading estimates that conflate illicit flows with poor data recording and harmonization practices. As a result, our policy recommendations begin with the simplest step- that all countries follow the General trade system and discard the Special trade system, to ensure minimizing source and destination reporting errors. To address commodity-level heterogeneity issues commonly faced by customs authorities, we recommend introducing more detailed product categories within the HS that reflect market realities e.g. a classification system for gold doré bars based on different levels of purity such as 30-50, 50-70, 70-90 percent. Global trade systems would also benefit greatly from harnessing new technologies such as blockchain, artificial intelligence, and mobile payments to improve tracking, optimize shipping routes, and reduce customs processing times respectively (World Economic Forum, 2018). Finally, there remains a crucial need for greater synchrony between the legal and economic definitions of illicit versus illegal financial flows. This is especially true for exports from developing countries such as Ghana that do not have clear, non-arbitrary guidelines that can help authorities distinguish between illicit and illegal flows.

While these measures would further harmonize aggregate trade statistics, we fully recognize that the identification of IFF-prone trade flows must be conducted through a micro-level analysis. Accordingly, we advocate a country-specific approach, which uses detailed customs data and explicitly accounts for the country’s characteristics in business practices, recording procedures and trade partner relations through expert interviews and secondary research before arriving at an estimation of IFFs in commodity-trade.

References

Bhagwati, J. N. (1974). On the underinvoicing of imports. In Illegal transactions in international trade (pp. 138-147). North-Holland.

Hong, K. P., & Pak, S. J. (2017). Estimating trade misinvoicing from bilateral trade statistics: The devil is in the details. The International Trade Journal, 31(1), 3-28.

Marur, S. (2019). Mirror-Trade Statistics: Lessons and Limitations in Reflecting Trade Misinvoicing. R4D-IFF Working Paper Series, R4D-IFF-WP04-2019. Download here.

Nitsch, V. (2016). Trillion dollar estimate: Illicit financial flows from developing countries (No. 227). Darmstadt Discussion Papers in Economics.

Fan, Z. & Chifelle, C. (2018). These 5 technologies have the potential to change global trade forever. Retrieved from

Photo by Adonyi Gàbor on Pexels

One thought on “Measuring IFFs: Lessons in Improving Methods”